In this series, I will walk you through the fundamentals of renewable energy project finance in Japan, using solar power projects as a practical example. Renewable energy projects are among the most common applications of project finance in Japan, and through a number of articles, I will explain how these projects are structured, financed, and operated, as well as the key legal and commercial issues involved.

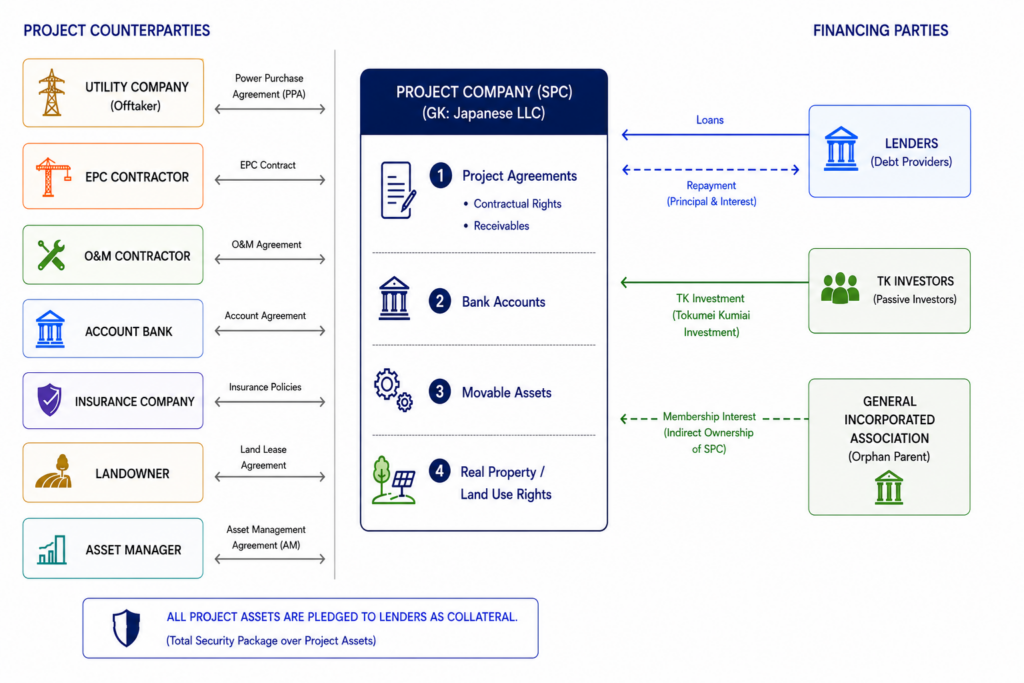

This diagram provides a concise overview of how solar power projects are typically structured and financed in Japan.

At the center of the structure is the GK (Godo Kaisha), which serves as the project company. A GK is a form of Japanese limited liability company and is widely used in Japanese project finance transactions.

There are several reasons why a GK is preferred as the project company. One of the most important is insolvency treatment. Unlike a stock company (Kabushiki Kaisha or KK), a GK is not subject to corporate reorganization proceedings under the Corporate Reorganization Act (Kaisha Kosei Ho). Instead, only civil rehabilitation proceedings under the Civil Rehabilitation Act (Minji Saisei Ho) are available. Because civil rehabilitation proceedings allow the debtor to remain in possession of the business and assets (debtor in possession), lenders typically view a GK as a more lender-friendly vehicle.

On the right side of the diagram are the financing parties.

First, lenders provide loans to the GK. In return, lenders take security over substantially all project assets, including project agreements, receivables, bank accounts, equipment, and land use rights. This is often referred to as the “all-assets security package.” In practice, the security package often extends beyond the assets owned directly by the project company and includes security over the equity interests in the project structure, such as the TK interests and the membership interest (Shain Mochibun) in the GK.

Second, TK investors make Tokumei Kumiai (TK) investments in the GK. The combination of a GK and TK investors is commonly known as the “GK-TK structure,” which is one of the most widely used investment structures in Japanese renewable energy projects.

TK investors are passive investors and, as a matter of law, are not permitted to participate in the management of the project. In practice, however, they often seek (indirect) control over the project. For example, they may appoint an affiliated asset manager under an asset management agreement or negotiate veto rights over key decisions under the TK agreement. One of the key advantages of the GK-TK structure is its tax efficiency. Distributions made by the GK to TK investors are generally treated as deductible expenses for Japanese tax purposes, allowing the structure to avoid the economic double taxation that might otherwise arise. However, it is important that the arrangement is respected as a bona fide TK arrangement. If the TK arrangement is not respected, one potential consequence is that it could be recharacterized as a general partnership (Nin-i Kumiai), which may result in less favorable tax treatment. That said, the actual tax consequences will depend on the specific facts and circumstances, including the tax residence and tax status of the relevant TK investors. Accordingly, tax advice should be obtained on a case-by-case basis.

Finally, at the bottom right is the General Incorporated Association (Ippan Shadan Hojin or ISH), which serves as the orphan parent of the GK. It is “orphan” because the ISH has no shareholders or other economic owners and is therefore legally independent from the sponsors and investors. In practice, however, the ISH is often established at the initiative of the sponsors or their advisors as part of the project structuring process. Accordingly, while the ISH is legally independent, it is not necessarily independent in a practical or commercial sense. By placing the GK under such an entity rather than under the direct ownership of the sponsors, the structure enhances bankruptcy remoteness and reduces the risk that the insolvency or financial distress of a sponsor could adversely affect the project company.

On the left side of the diagram are the project counterparties. In many Japanese renewable energy projects, (affiliates of) the TK investors are often involved in the project not only as investors but also as service providers. For example, an affiliate of a TK investor may act as the EPC contractor, O&M provider, or asset manager (AM), thereby participating in the development, operation, and management of the project.

These project agreements are generally pledged as part of the lenders’ security package. They also typically include limited recourse and non-petition provisions. Furthermore, to facilitate a lender step-in following a default under the financing documents, the parties often enter into a conditional assignment arrangement pursuant to which the lenders may designate a replacement project operator and have the relevant project agreements transferred to such operator upon enforcement of the security.